Investment strategies with ETFs

Fee settings

Basic strategy

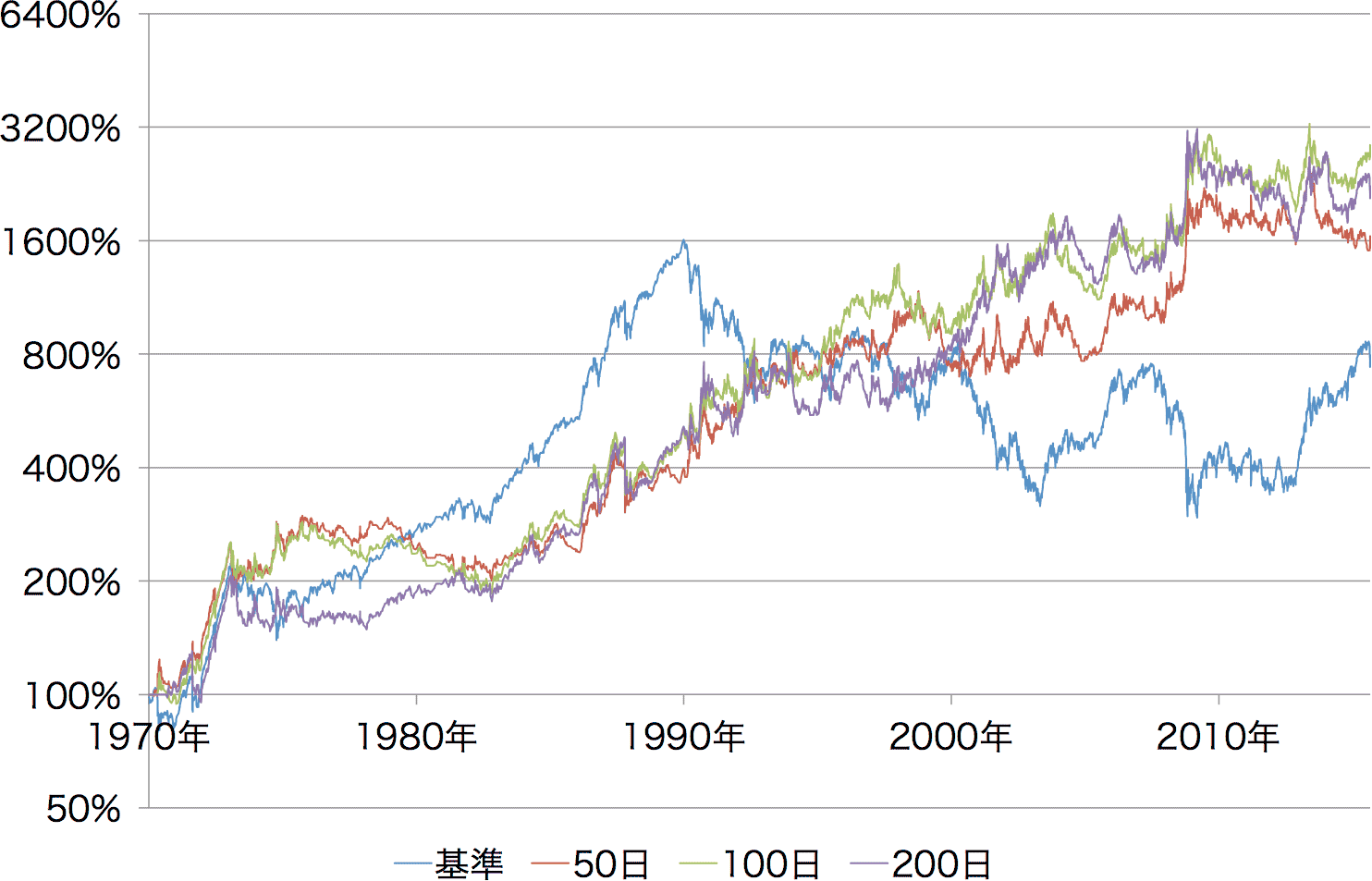

Figure 1: ETF investment simulation

(slack 2%, fee 0.15%, leverage ±1x)

(slack 2%, fee 0.15%, leverage ±1x)

Appendix

- Long-term investment strategies using the Nikkei Stock Average … the previous article

- SBI Securities fees … basis for the fees