Formulating exchange rate fluctuations

Examining fluctuations by time of day

Differences between years

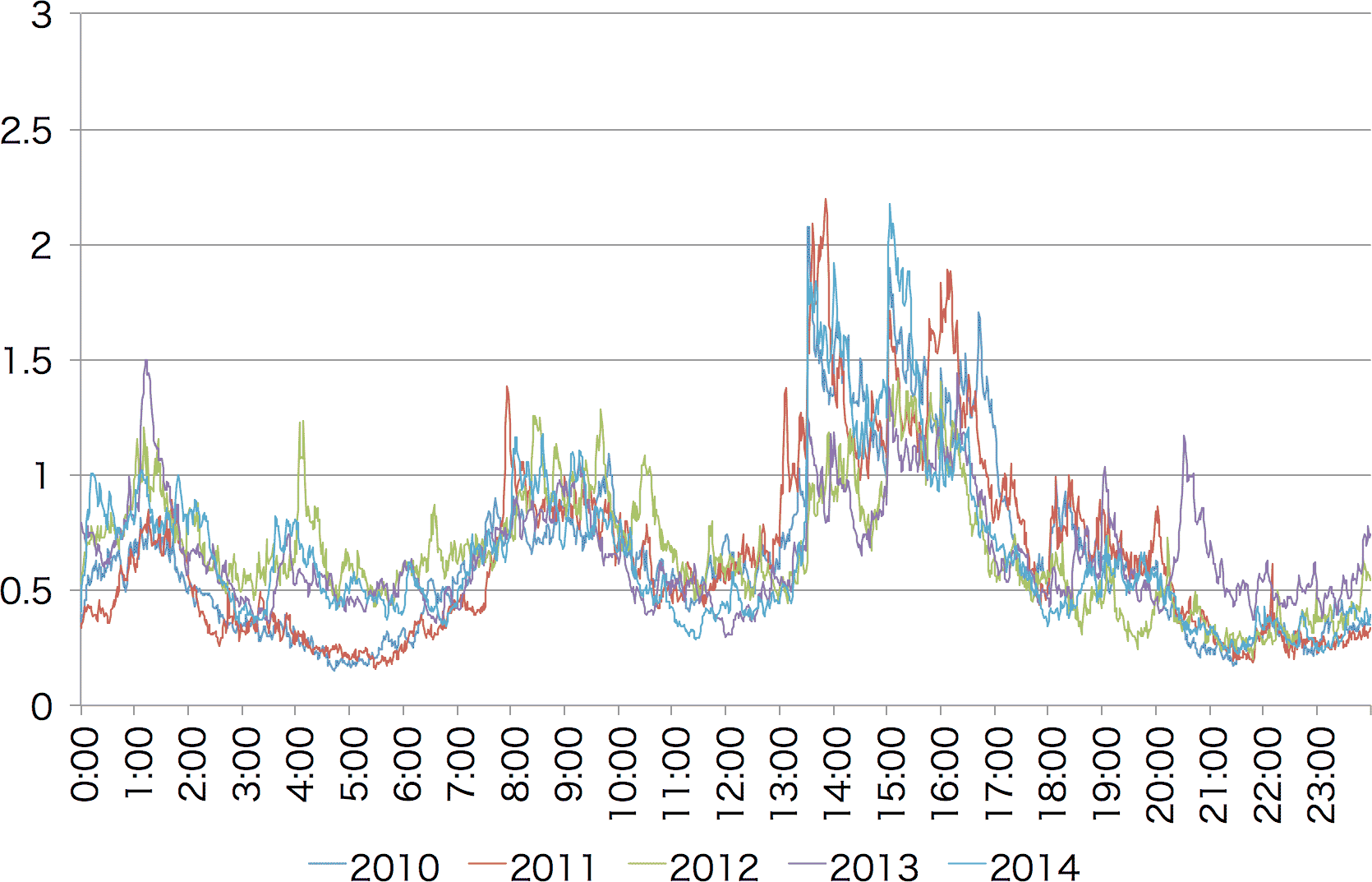

Figure 1: Fluctuation of USD/JPY by time of day during winter time, 2010–2014

(the X axis is the time in UTC, the Y axis is the amount of fluctuation)

(the X axis is the time in UTC, the Y axis is the amount of fluctuation)

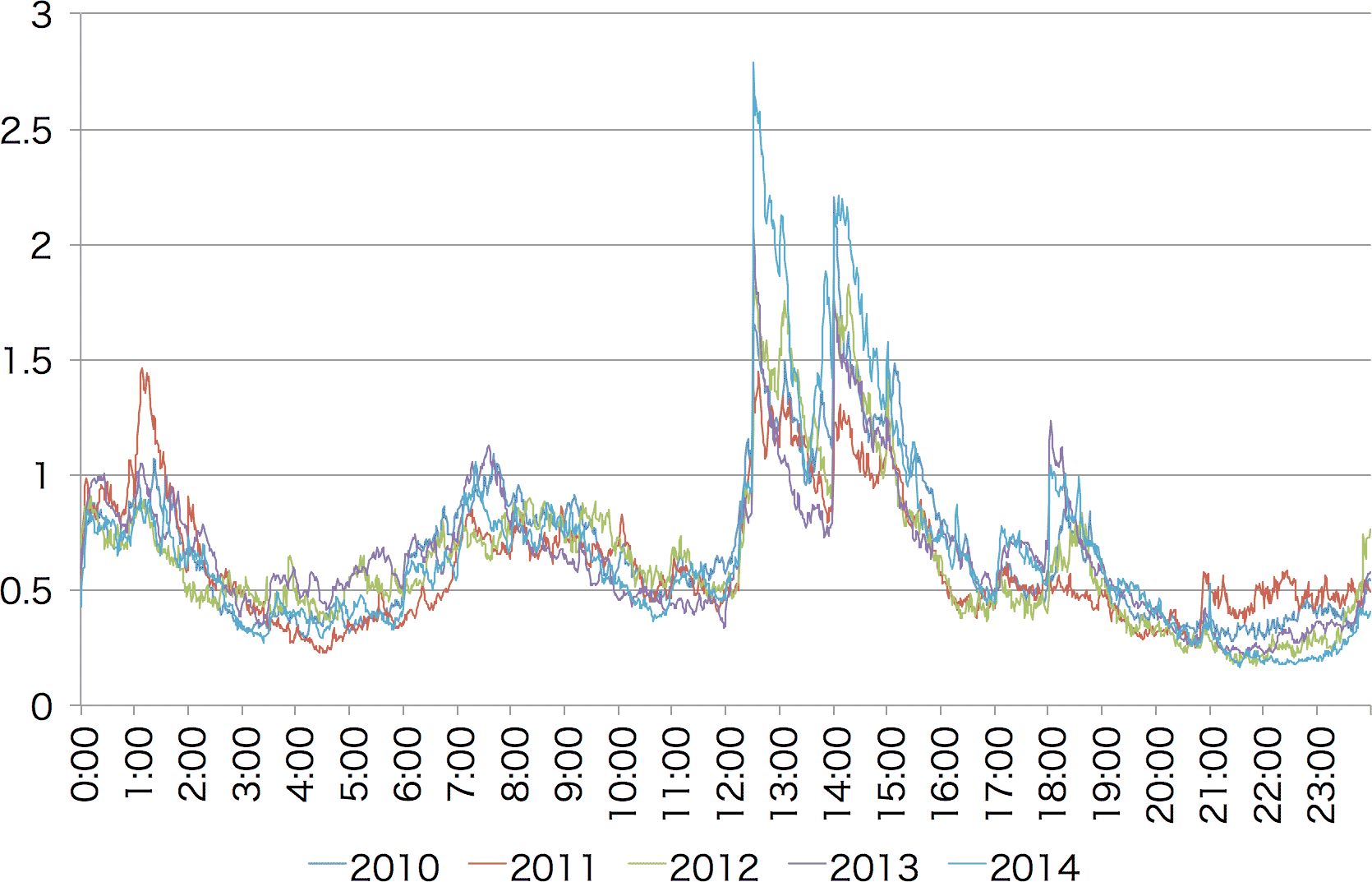

Figure 2: Fluctuation of USD/JPY by time of day during summer time, 2010–2014

(the X axis is the time in UTC, the Y axis is the amount of fluctuation)

(the X axis is the time in UTC, the Y axis is the amount of fluctuation)

Differences by day of the week

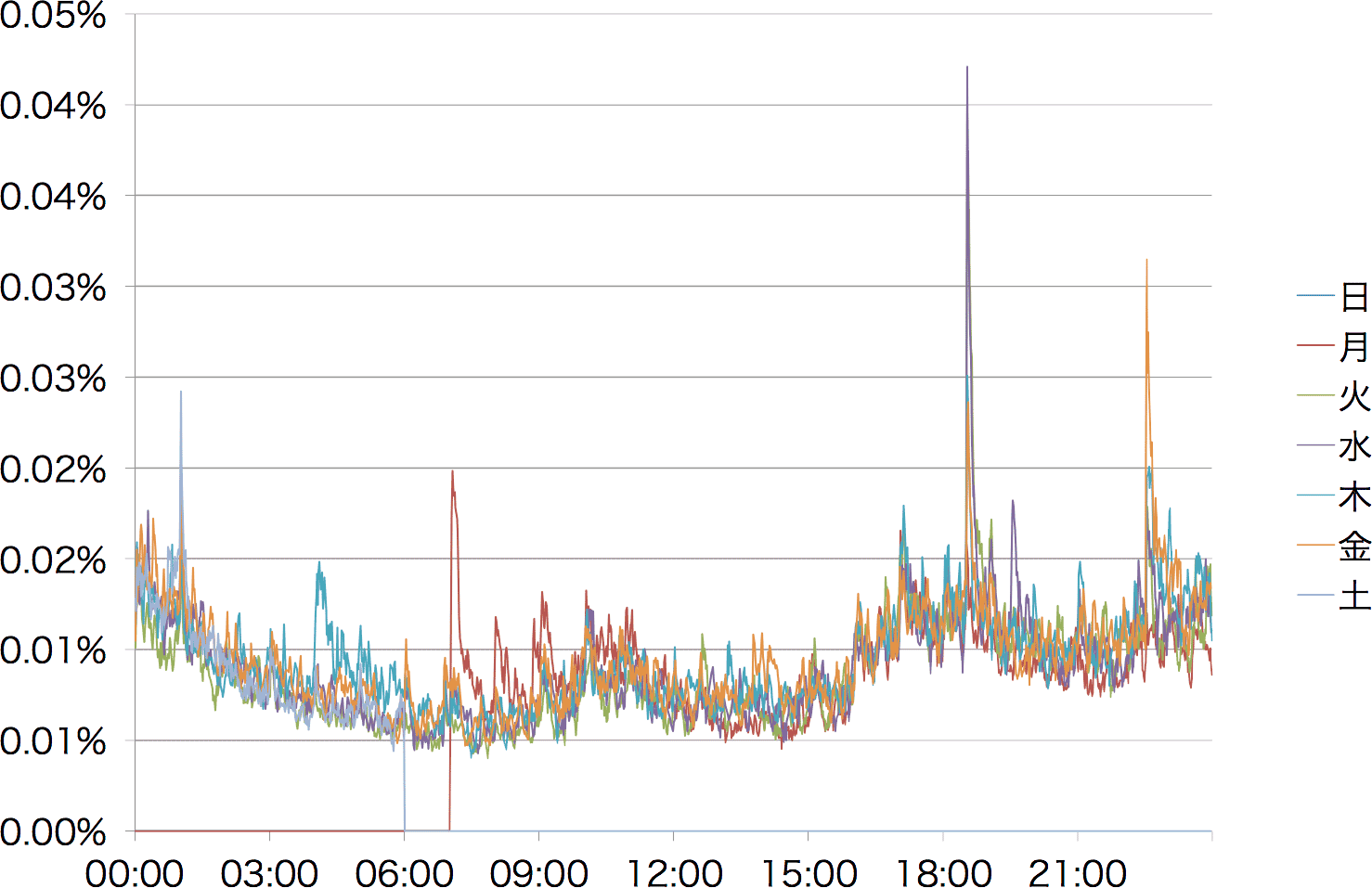

Figure 3: Weekly fluctuation of GBP in 2014

(the X axis is the time, the Y axis is the amount of fluctuation)

(the X axis is the time, the Y axis is the amount of fluctuation)

- 7:00 to 10:00 on Monday … fluctuations that absorb the potential real-economy changes over the weekend

- 18:30 … fluctuations from the release of UK economic indicators

- 22:30 … fluctuations from the release of US economic indicators

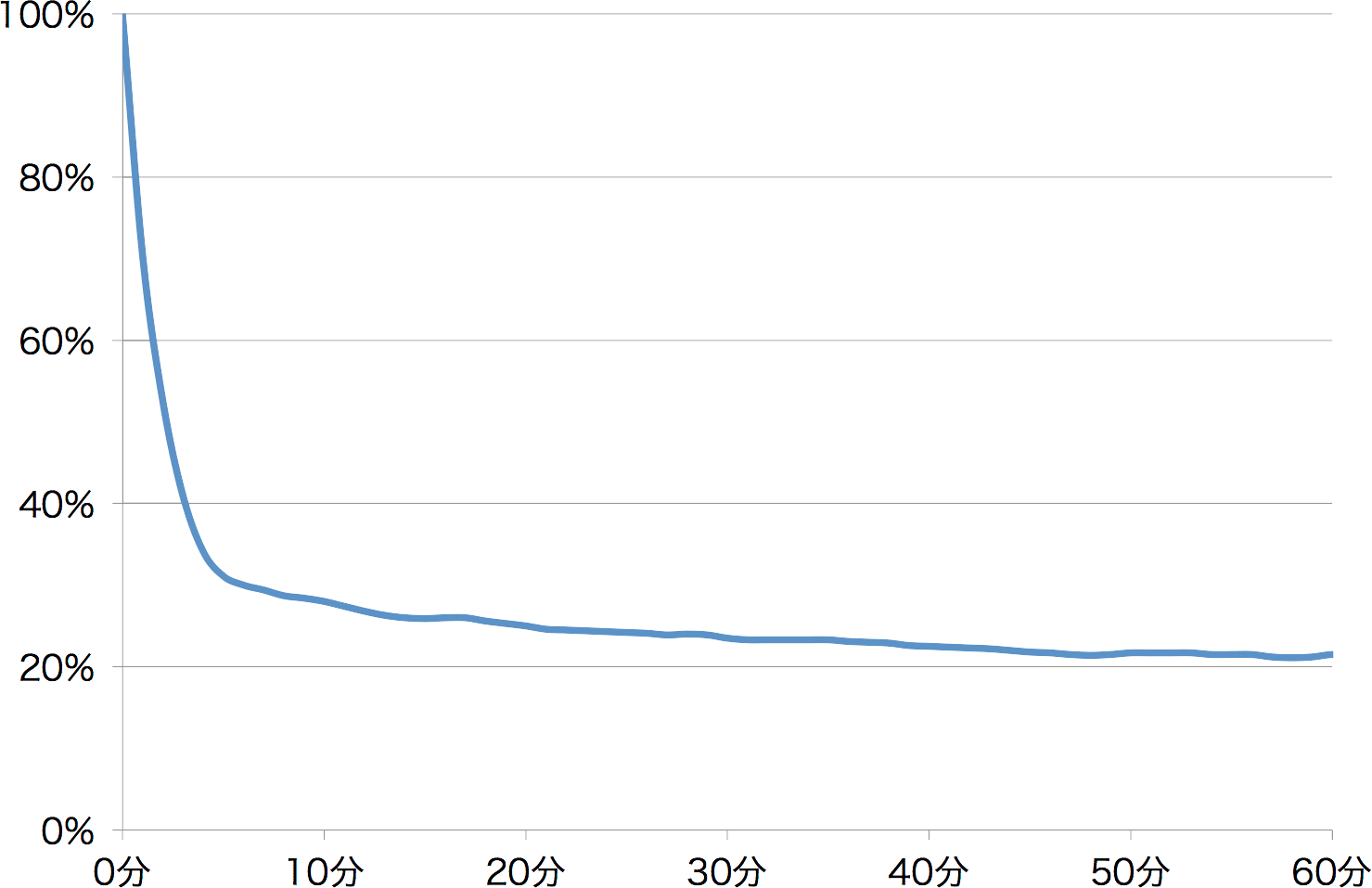

Examining time and fluctuation scale

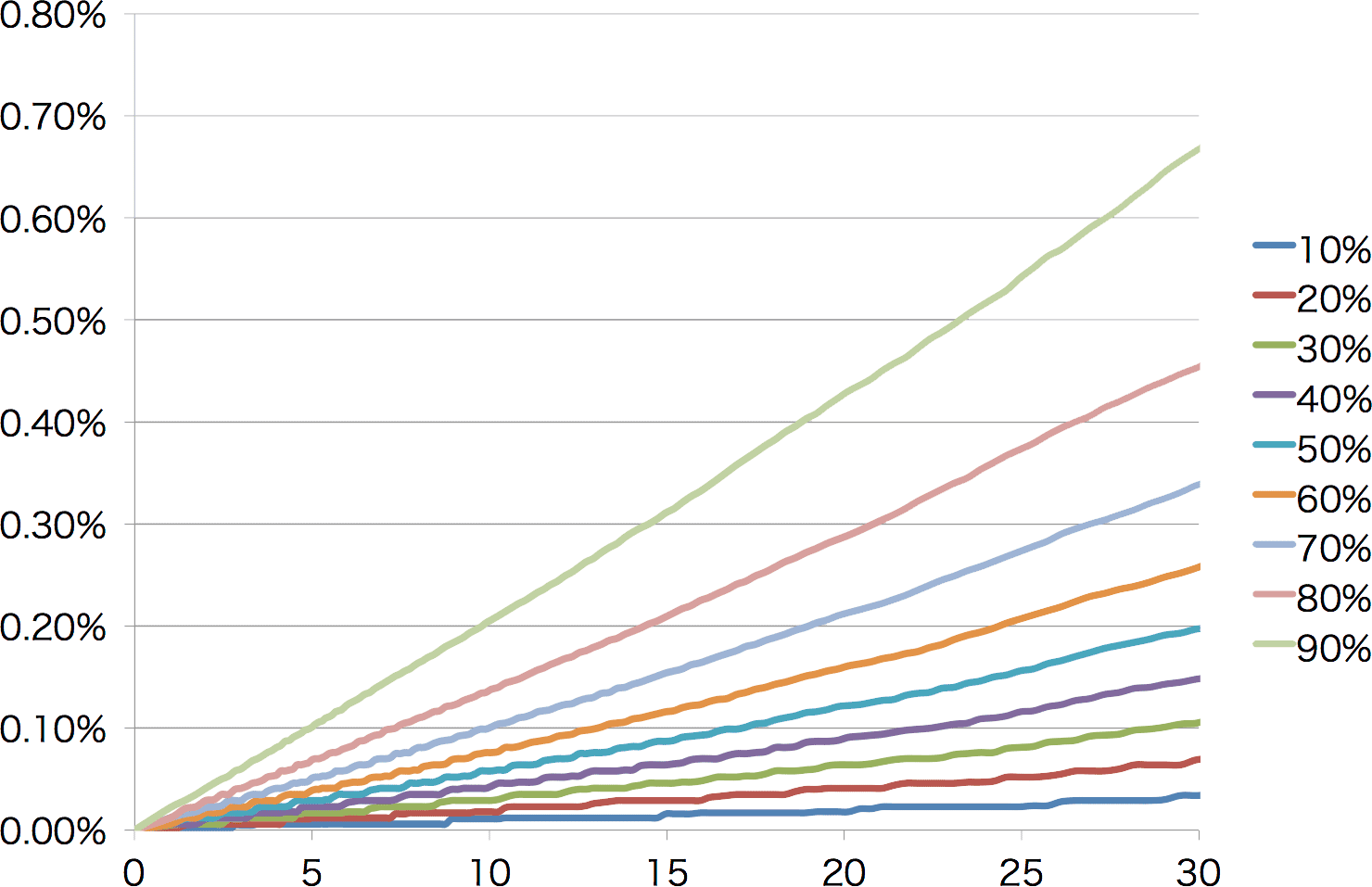

Figure 4: Fluctuation of GBP in 2014

(the X axis is the square root of the target time in minutes, the Y axis is the amount of fluctuation, and each series is the amount of fluctuation that falls within that percentile)

(the X axis is the square root of the target time in minutes, the Y axis is the amount of fluctuation, and each series is the amount of fluctuation that falls within that percentile)

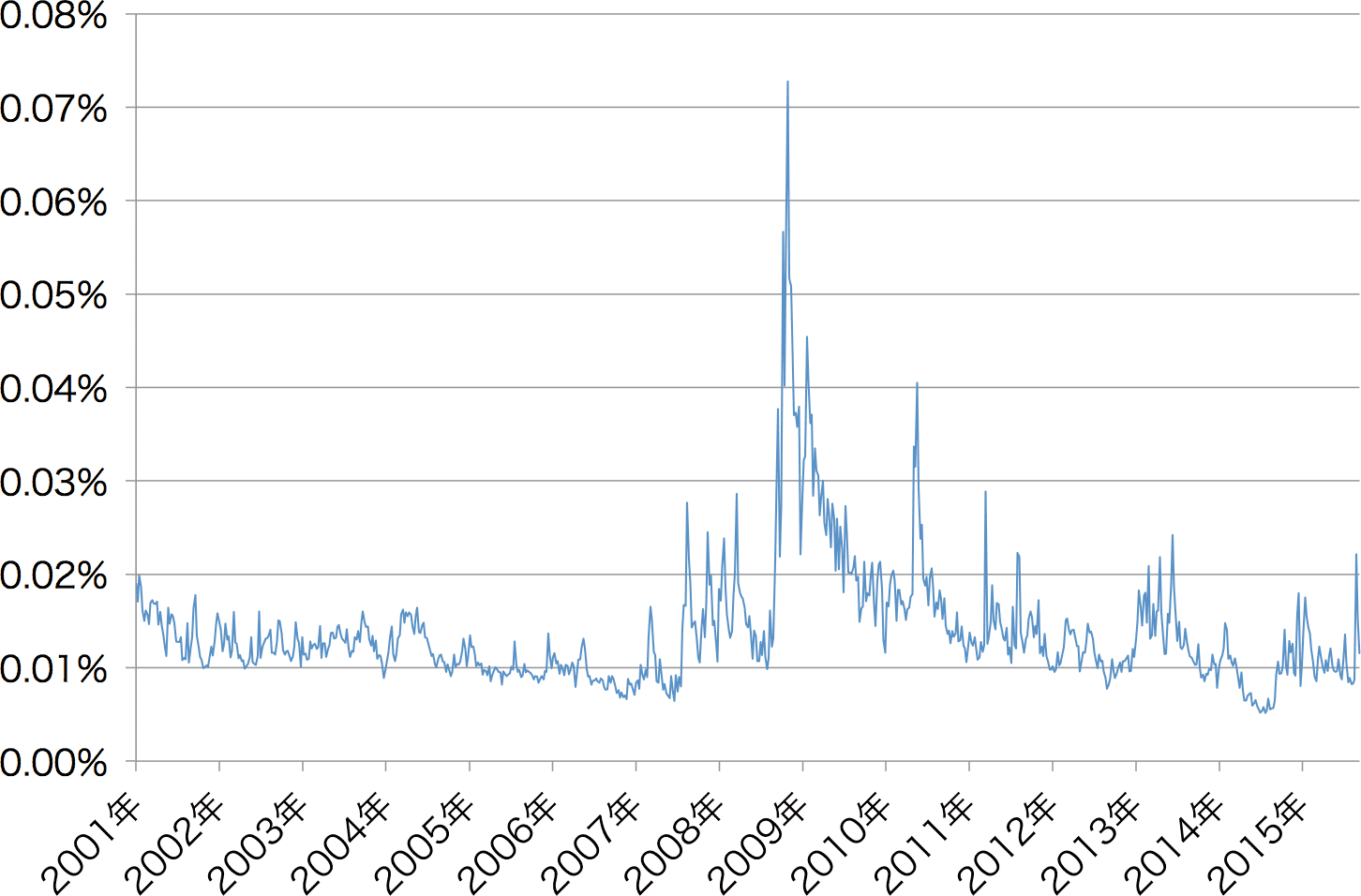

Examining fluctuations over time series

Figure 5: Fluctuation of GBP, 2001–2015

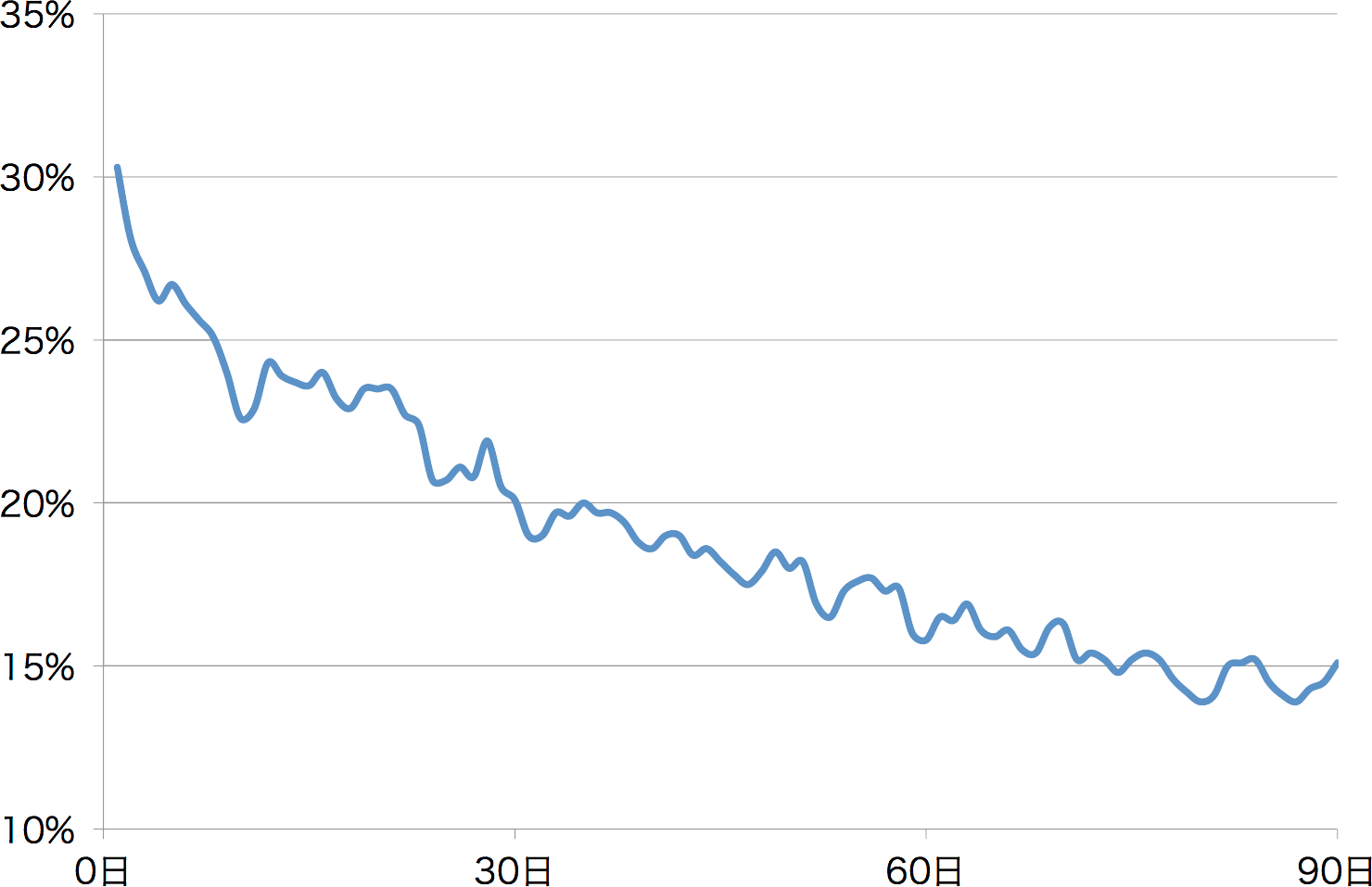

Autocorrelation of exchange rate fluctuations

Figure 6: Short-term autocorrelation of GBP in 2014

(the X axis is the time difference, the Y axis is the amount of fluctuation)

(the X axis is the time difference, the Y axis is the amount of fluctuation)

Figure 7: Long-term autocorrelation of GBP, 2001–2014

(the X axis is the time difference, the Y axis is the amount of fluctuation)

(the X axis is the time difference, the Y axis is the amount of fluctuation)