Imos Financial Theory

0. Introduction: How Imos Financial Theory Differs from Orthodox Financial Theory

- As the evaluation function U(x) for investments carrying a distribution (in the language of financial theory, the utility function), we use precisely {\rm ln}(x), and we believe its expected value should be maximized. When performing portfolio optimization, the orthodox school often fixes the expected return (or the volatility) and, within that, minimizes the volatility (or maximizes the expected return) (e.g., Modern portfolio theory - Wikipedia). But from the idea that investors should not fix those quantities but rather take on risk that is worth it, we believe that what should be optimized is the size of the expected return relative to risk. Financial theory too sometimes optimizes the size of the expected return relative to risk by using risk-averse utility functions or the Sharpe ratio, but among these we believe that the logarithmic utility function in particular should be used because of its good properties.

- As for how to hold financial instruments, we believe that the ratio of each financial instrument to one's own assets (the leverage) should be held fixed. Orthodox financial theory often either limits the quantity of a financial instrument by one's assets, or assumes unlimited borrowing subject to some other constraint, and assumes that over a short period the quantity of the instrument is not changed. But we consider that in reality this has problems—such as being able to trade up to the maximum leverage in margin/credit transactions, and being unable to adequately represent long periods that include rebalancing—so, as a trading model that can be expressed in continuous time including rebalancing, we take the position that "the ratio of each financial instrument to one's own assets (the leverage) should be held fixed."

1. Financial Model

1.1. Price-Fluctuation Model of Financial Instruments

1.1.1. Price-Fluctuation Model of Financial Instruments

1.1.2. Continuous Price-Fluctuation Model of Financial Instruments

1.1.3. Expected Value and Variance of the Price of a Financial Instrument

1.2. Model of Financial Trading: A Model That Applies Leverage on Finite Assets

1.2.1. Asset-Fluctuation Model Under Leverage

In the case of margin trading, borrowing is not structurally necessary, but in the case of spot or credit trading, when L \gt 1 there is a shortfall of V(L-1) in cash, which we assume is handled by borrowing.

1.2.2. Expected Value and Variance of Assets Under Leverage

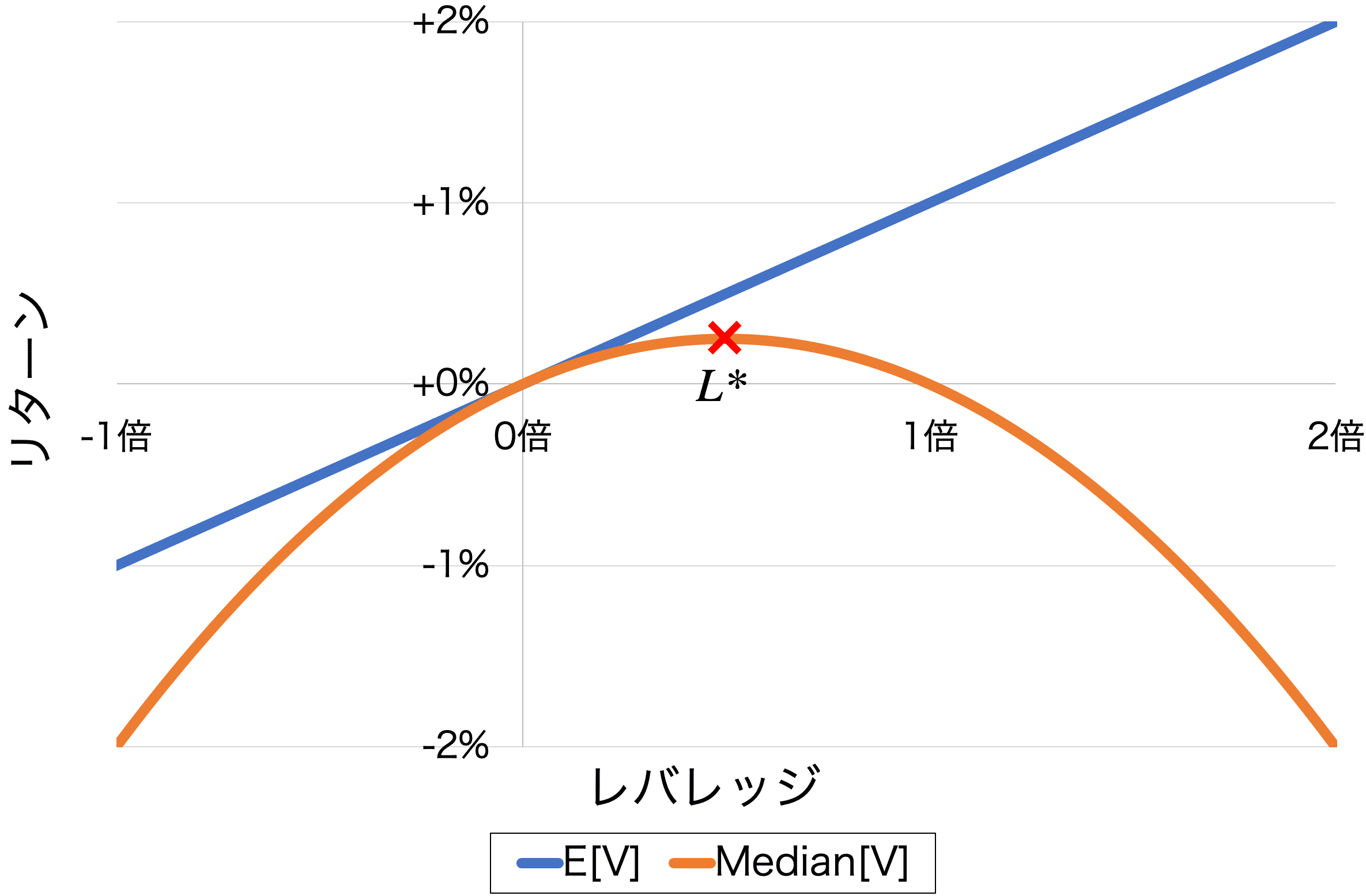

1.2.3. Decay of the Median Due to Leverage

Figure 1.2.3: Relationship between leverage and return for the expected value and the median

1.2.4. Why We Use a Logarithmic Utility Function

2. Portfolio Optimization

3.1. Portfolio Optimization with Two Uncorrelated Assets

2.2. Portfolio Optimization with Multiple Correlated Assets

3. Fluctuation Model of Foreign Exchange

3.1. Fluctuation Model of Foreign Exchange

- When currency A becomes \exp(d) times currency B, the order of people in country A becomes \exp(d) times and takes profit, while the order of people in country B becomes \exp(-d) times and cuts loss.

- When currency A becomes \exp(-d) times currency B, the order of people in country A becomes \exp(-d) times and cuts loss, while the order of people in country B becomes \exp(d) times and takes profit.

3.2. Introducing the True Value

3.2.1. Fluctuation of a Currency Relative to the True Value

3.2.2. Three or More Currencies

3.2.3. Currencies with Different Volatilities

4. Conclusion

- As shown in Section 1.1.2, the price of a financial instrument that can be expressed using the Black–Scholes equation can be represented by a log-normal distribution.

- As shown in Section 1.2.3, applying high leverage greatly reduces the median return.

- As shown in Section 1.2.4, Imos Financial Theory uses the logarithmic utility function U(x)={\rm ln}(x). This coincides with optimizing so as to maximize the median of the price of a financial instrument that follows a log-normal distribution.

- As shown in Section 1.2.4, the optimal leverage L^* that maximizes the median is obtained using the price S of the financial instrument as follows.

- As shown in Section 2.1, the optimal portfolio of multiple independently fluctuating assets coincides with the optimal leverage of each individual asset.

- As shown in Section 2.2, the optimal portfolio of multiple correlated assets is obtained using the expected-return vector μ and the covariance matrix Σ as follows.

- As shown in Section 3.1, in an environment where one can trade only a single foreign currency as stable as one's own, if one wishes to maximize the log expected utility of assets, this can be achieved by holding it at leverage 0.5 (half of the asset valuation in the foreign currency).